Clear Sky Science · en

Consumer credit evaluation model for free trade ports by a sparse attention transformer and graph neural network

Why smarter credit checks matter

Every time you swipe a card or buy something online, a hidden system decides whether to trust you. In fast-growing free trade ports—busy hubs for cross-border shopping and finance—millions of such decisions happen every day. Traditional credit checks, built for slower, simpler economies, struggle to keep up with today’s nonstop, highly connected digital transactions. This study explores a new artificial intelligence approach that can sift through huge streams of payment behavior and tangled webs of shared devices and internet addresses to spot who is likely to default—and who is simply a normal customer.

From simple scores to living financial footprints

Conventional credit scoring often treats people as if their financial lives were frozen snapshots: a few numbers about income, balances, and past debts. That view breaks down in free trade ports, where shoppers leave long, detailed trails of purchases, refunds, and cross-border payments. Here, risk changes over months or years, not in a single moment. The authors argue that understanding creditworthiness now requires reading a “movie” of behavior rather than a still photo, and also recognizing that one person’s risk can spread through networks of shared devices, addresses, and online accounts.

Two digital lenses on the same customer

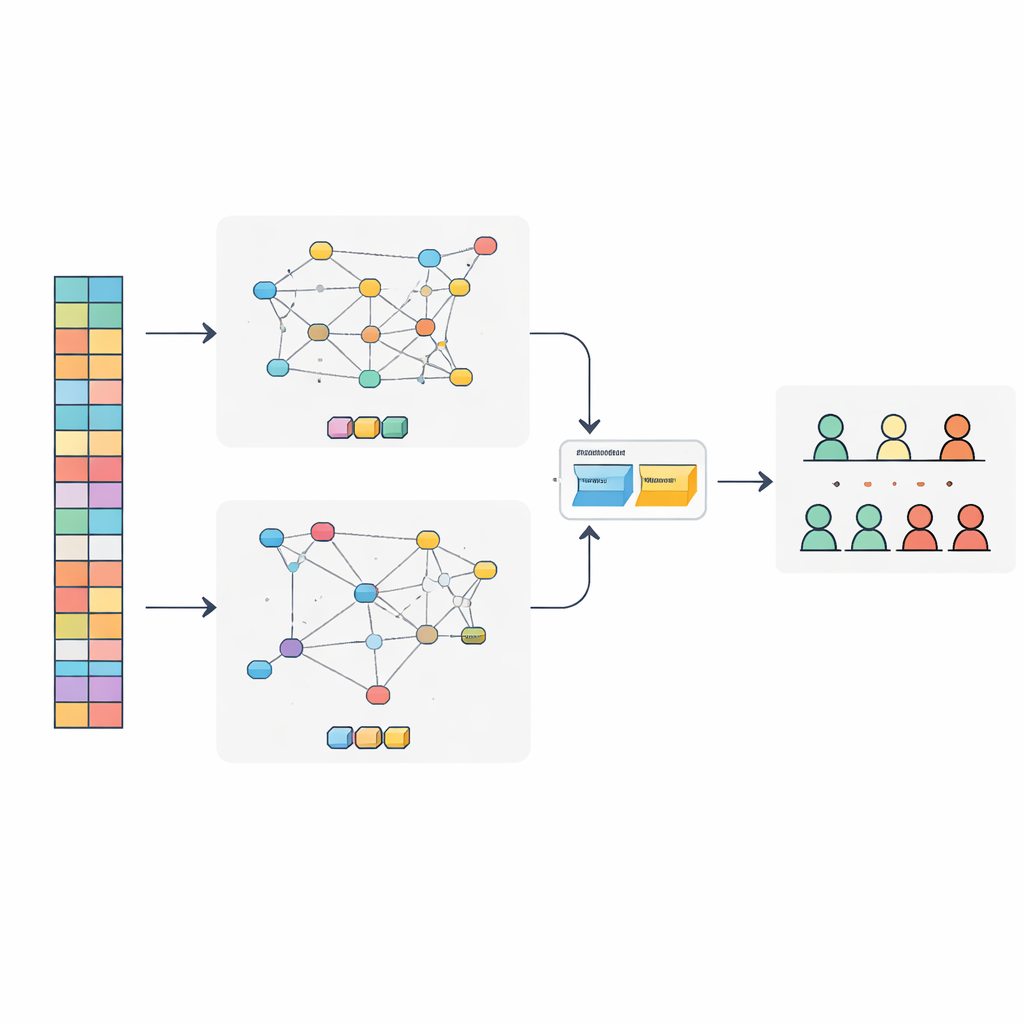

The researchers created a combined model, called SAT-GNN, that looks at each consumer from two complementary angles. The first angle is time: it follows very long chains of transactions for each person, sometimes thousands of steps long. To do this efficiently, the model uses a modern attention-based method that focuses computing power on the most informative moments instead of treating every purchase equally. The second angle is relationships: it builds a network linking consumers to the phones, computers, IP addresses, and email domains they use. Clusters of accounts that quietly share the same hardware or network environment can reveal hidden groups, including possible fraud rings.

How the model blends behavior and connections

Inside SAT-GNN, one branch specializes in reading the transaction timeline, while another specializes in understanding the risk signals carried by the network of linked entities. Instead of simply stapling these two views together, the authors add an adaptive fusion layer that learns how much weight to give each one for every case. For customers with long, stable histories, the behavior branch can dominate. For newcomers with little history but many connections to risky devices or addresses, the network view can take the lead. This flexible balance helps the system stay reliable even when data are sparse or unusually distributed.

Putting the new system to the test

To see whether SAT-GNN actually works better than widely used tools, the team tested it on a large public dataset of online transactions commonly used for fraud and risk research. They compared it with popular models used in the finance industry, such as gradient boosting methods and standard deep learning sequence models. SAT-GNN achieved higher scores on several key measures, including the ability to rank risky customers correctly and to catch a larger share of true defaulters. It was especially strong when transaction histories were long and when relational patterns—like groups of accounts sharing devices—played an important role. At the same time, the system could make decisions in just a few milliseconds, fast enough for real-time use.

What this means for everyday borrowers

For non-specialists, the take-home message is that credit checks are becoming more like sophisticated pattern recognition than simple rule-following. By jointly reading a person’s long-term spending story and their hidden connections to others, SAT-GNN offers lenders in free trade ports a sharper and quicker way to tell routine customers apart from truly risky ones. That can reduce losses from fraud and default while also making it easier to extend credit fairly and efficiently to legitimate borrowers. The study suggests that future financial systems will increasingly rely on such dual-view, adaptive models to keep pace with the complexity of modern digital commerce.

Citation: Wu, M., Sabri, M.F., Meng, C. et al. Consumer credit evaluation model for free trade ports by a sparse attention transformer and graph neural network. Sci Rep 16, 10602 (2026). https://doi.org/10.1038/s41598-026-46849-4

Keywords: credit risk, free trade ports, deep learning, fraud detection, financial networks