Clear Sky Science · en

Interpretable ESG–sentiment hybrid deep learning for asset return forecasting with quantified interactions and latency-aware deployment

Why Markets Need More Than Price Charts

Anyone who has watched markets swing wildly knows that prices alone rarely tell the full story. Company behavior on the environment and society, as well as the daily mood of investors on news and social media, all leave their fingerprints on returns. This paper explores how to combine those scattered clues into a single, transparent forecasting system that aims not only to predict tomorrow’s move in stocks and cryptocurrencies, but also to show when sustainability credentials matter more than breaking headlines—and to do it fast enough for real-world trading.

Bringing Many Signals Under One Roof

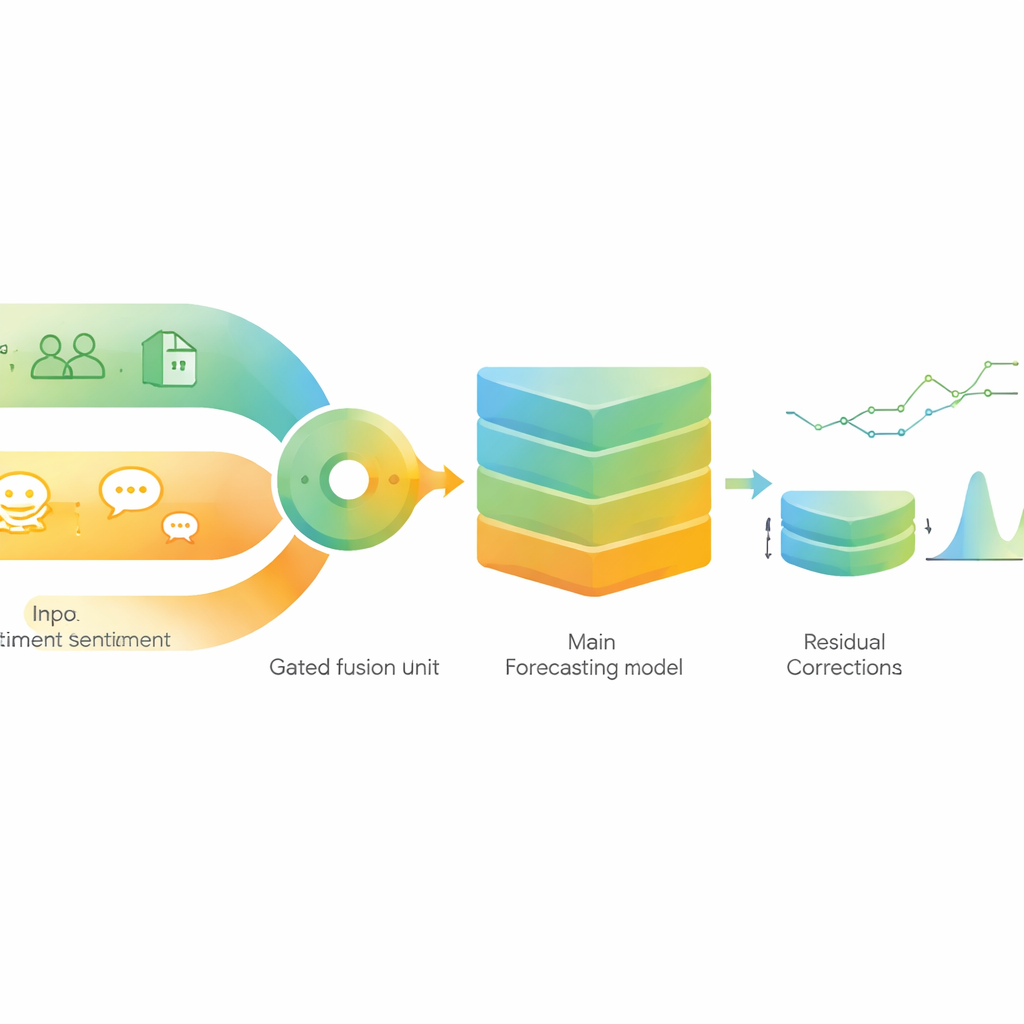

The authors build a hybrid forecasting pipeline that ingests four main types of information: standard market indicators from price and volume, broad economic data, firm-level environmental, social and governance (ESG) scores, and detailed sentiment extracted from financial news using a language model tailored to finance. The core engine is a modern sequence model that specializes in learning patterns over time. On top of this, a lighter-weight regression model acts like a second opinion, cleaning up leftover errors when market conditions shift. The goal is a compact system that is accurate, relatively easy to deploy, and open to inspection rather than a black box.

Letting Sustainability and Mood Take Turns

A central idea is that sustainability and sentiment do not matter equally at all times. To capture this, the model does not simply stack ESG scores and news mood side by side. Instead, it passes each through its own small processing block and then blends them using a “gate” that can lean more heavily on one or the other each day. When markets are calm, the gate can give more weight to steady, slow-moving ESG information. During storms, it can swing toward fast-changing news sentiment. The researchers then use modern explanation tools to measure, in a statistically rigorous way, how strongly ESG and sentiment interact and how that balance shifts across different volatility regimes.

Testing Through Booms, Busts, and Crypto Swings

To see whether the approach holds up outside of hand-picked examples, the authors run a strict walk-forward test from 2020 to 2024 on large U.S. technology stocks, major global indices, and Bitcoin and Ethereum. They train on roughly one year of data at a time and test on the following two weeks, always respecting realistic delays in when news, ESG updates, and macro figures become known. They compare their system with a range of popular deep learning and machine learning models, including a finance-focused large language model that reads news directly. Across many random restarts and assets, their hybrid model reduces forecast error, gets the direction of the next-day move right more often, and improves risk measures such as information ratios.

What Happens in Crisis Periods

The study pays special attention to turbulent periods, including the COVID-19 crash, the 2022 interest-rate tightening cycle, and the 2023 banking stress, as well as generic high-, medium-, and low-volatility phases. As expected, everyone’s errors grow when markets lurch, but the hybrid model still retains an edge. A simple long-only trading rule based on its forecasts earns higher risk-adjusted returns and suffers smaller drawdowns than a strong text-only benchmark, even after conservative transaction costs. Analysis of the gate and interaction measures shows a clear pattern: during stressed, high-volatility windows the system leans more on sentiment, while in quieter, low-volatility markets it shifts weight back toward ESG, consistent with the idea that panic and euphoria dominate the short term, whereas resilience and governance matter more in the long run.

Fast Enough for Live Use

Because real trading systems care about speed as well as accuracy, the authors also design a trimmed-down version of their model that removes heavier auxiliary components while keeping the core logic intact. This latency-aware variant keeps over ninety percent of the accuracy gains but cuts inference time by roughly half, making it more suitable for near real-time decision-making. Importantly, the interpretability tools—showing how ESG and sentiment interact and how residual errors are stabilized—still work for this lighter model, preserving transparency.

What This Means for Everyday Investors

For a lay reader, the key takeaway is that combining how a company behaves (its ESG profile) with how people feel about it (news sentiment) can yield more stable and informative forecasts than either source alone, especially when done in a way that adapts to market conditions and is carefully checked for statistical soundness. The proposed framework does not promise effortless profits, and it does not prove that ESG causes better performance. But it does show that sustainability and crowd mood contain complementary, regime-dependent information that can be harnessed in a clear and efficient way, offering a more nuanced lens on risk and return in modern, news-saturated markets.

Citation: Mishra, S., Mayaluri, Z.L., Liew, C.Y. et al. Interpretable ESG–sentiment hybrid deep learning for asset return forecasting with quantified interactions and latency-aware deployment. Sci Rep 16, 12001 (2026). https://doi.org/10.1038/s41598-026-41985-3

Keywords: financial forecasting, ESG investing, news sentiment, hybrid deep learning, market regimes