Clear Sky Science · en

Electric power data element trading price prediction model based on improved grid VMD Resnet-BiLSTM algorithm

Why tomorrow’s power price matters to you

Whether you run a factory, manage a wind farm, or just pay a household bill, the price of electricity shapes daily life and long‑term planning. As more wind and solar power flow into modern grids, prices swing up and down more sharply and less predictably than in the past. This study presents a new way to forecast day‑ahead electricity prices more accurately and more reliably, helping market operators, generators, and consumers make smarter decisions in a cleaner but more volatile energy system.

Power from sun and wind, and the new price roller coaster

The authors focus on a real power system in New South Wales, Australia, where solar and wind supply a large share of electricity and two high‑capacity transmission lines help smooth imbalances. Because electricity must be produced the instant it is used, sudden clouds, calm winds, or demand spikes can send prices soaring or crashing within minutes. Traditional statistical tools and basic machine‑learning models struggle with this kind of noisy, highly nonlinear behavior. They either miss long‑term patterns, such as daily and seasonal cycles, or fail to keep up with rapid, short‑term jumps. The paper asks how to design a forecasting system that can see both the broad trends and the fine‑grained jolts in price data.

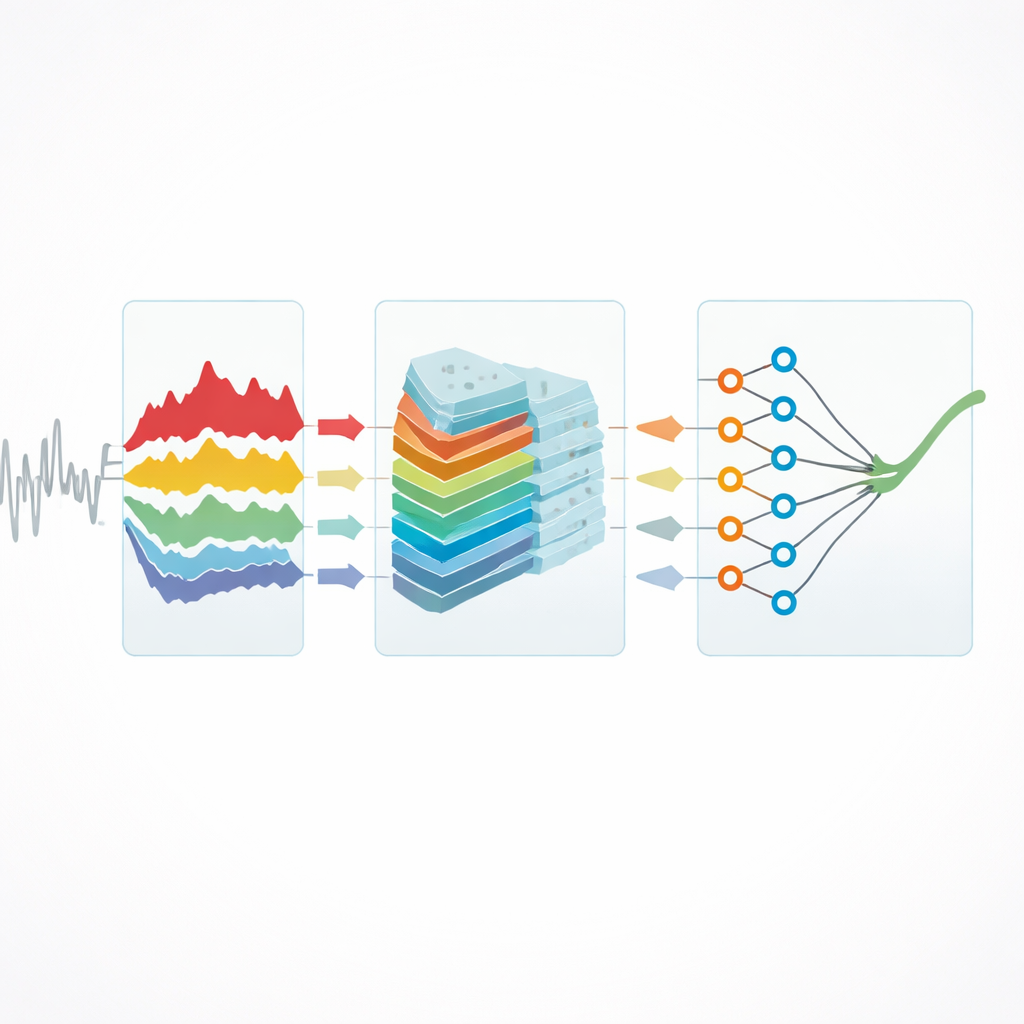

Breaking a messy signal into clearer pieces

The first step in the proposed method is to cleanly separate the tangled movements of the price signal. The researchers use a technique called variational mode decomposition to split the original price series into a handful of simpler components, each representing a different rhythm of change—from slow swings over seasons to quick spikes driven by sudden events. They then tune this decomposition with a statistic that measures how strongly each component is related to known driving factors, such as demand and weather. By searching over possible settings and choosing those that maximize this measure of mutual dependence, they ensure that each extracted component carries real information about how and why prices move, rather than random noise.

Teaching a deep network to focus on what matters

Once the price series has been peeled into several cleaner layers, the authors feed these layers into a deep‑learning structure that combines two powerful ideas. A residual shrinkage network uses a series of small convolutional filters and adjustable thresholds to highlight informative patterns and push unhelpful fluctuations toward zero. This produces a compact “feature map” that keeps key signals while discarding much of the clutter, which both improves learning and reduces the computational burden. These refined features are then passed to a bidirectional recurrent network that reads the time series forward and backward. By looking at both past and future context within the training data, this network can better capture how price changes build up and unwind over time.

Putting the model to the test in the real world

The team trains and validates its model on five years of half‑hourly Australian price data, using 2020–2022 for training, 2023 for tuning, and 2024 for testing. They carefully handle missing values and outliers and compare their approach with several advanced competitors, including other decomposition‑plus‑deep‑learning hybrids and a model based on generative techniques. Across standard error measures, the new model cuts forecasting mistakes to a fraction of those from rival methods; for example, its average percentage error over the year is well under 1%, while others are several times higher. It maintains this edge across all four seasons, during the most turbulent “worst‑case” days, under added artificial noise, and even when applied to another Australian region without retraining, indicating strong robustness and generalization.

From better forecasts to steadier markets

For non‑specialists, the key message is that smarter math and machine learning can turn chaotic price data into a clearer, more predictable picture. By first separating long‑term trends from short‑term jolts and then using a tailored deep‑learning architecture to concentrate on the most informative patterns, the model delivers very accurate and stable day‑ahead electricity price forecasts. This level of precision can support fairer bidding, more confident investment in renewables, and better risk management for both large players and everyday consumers. As grids worldwide absorb more variable wind and solar power, approaches like this one may become essential tools for keeping electricity markets both efficient and reliable.

Citation: Zheng, Y., Huang, K.Q., Liu, J. et al. Electric power data element trading price prediction model based on improved grid VMD Resnet-BiLSTM algorithm. Sci Rep 16, 13720 (2026). https://doi.org/10.1038/s41598-026-40245-8

Keywords: electricity price forecasting, renewable energy integration, deep learning, time series decomposition, energy market stability