Clear Sky Science · en

Carbon price fluctuation forecasting using an adaptive dual-channel residual attention neural network optimized with white shark optimizer and blockchain-based data provenance

Why carbon price forecasts matter to everyday life

Carbon markets are one of the main policy tools for tackling climate change. They put a price on greenhouse gas emissions, nudging companies to pollute less and invest in cleaner technologies. But the prices in these markets swing up and down in complicated ways, making it hard for businesses, investors, and governments to plan ahead. This study presents a new way to forecast carbon prices more accurately and reliably, aiming to make climate-related financial decisions less of a guessing game.

The problem of wild carbon price swings

Carbon trading schemes let companies buy and sell emission allowances, effectively turning pollution into a tradable commodity. When prices are too volatile, firms struggle to budget for future costs, and policymakers find it harder to design stable climate rules. Carbon prices are influenced not only by basic supply and demand, but also by shifting regulations, energy prices, economic cycles, and even news sentiment. These forces make price movements highly nonlinear and noisy, so traditional forecasting methods often miss turning points or react too slowly to shocks.

Limits of current forecasting tools

Researchers have tried many advanced methods to tame this complexity, from breaking price series into smoother sub‑signals to using deep learning models and bio‑inspired optimization algorithms. Decomposition methods help reduce noise by splitting a price series into several components, which are forecast separately and recombined. Deep learning models, such as hybrid combinations of convolutional and recurrent networks or Transformer‑style architectures, can capture intricate time patterns. Metaheuristic optimizers, inspired by animal swarms or predators, search for good model settings beyond simple gradient descent. However, existing approaches usually tackle only part of the problem: they may handle either noise, or complex patterns, or optimization, but rarely all three together. They also tend to overlook the reliability and traceability of the underlying market data.

A combined pathway from data to trustworthy forecasts

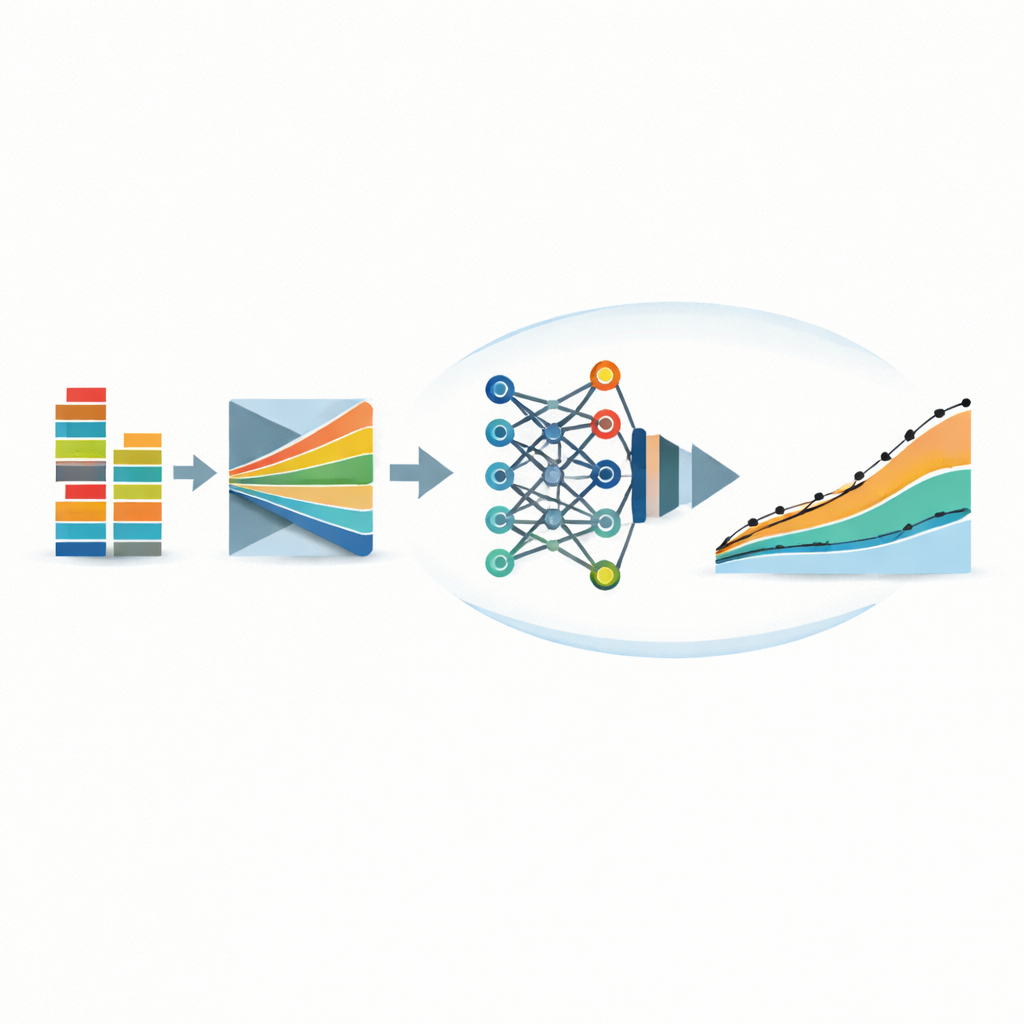

The authors propose an integrated framework called ADRGPNN‑WSO that links several ideas into one pipeline. First, raw daily trading data from three major Chinese carbon exchanges (Hubei, Shanghai, and Shenzhen) are cleaned using a fuzzy matching method that fills in missing values and downplays outliers. At the same time, the raw records are anchored on a special kind of blockchain designed to allow carefully controlled corrections while preserving a cryptographic audit trail. Only records whose digital fingerprints match the blockchain are allowed into the model, ensuring that the forecasts rest on trustworthy data rather than tampered inputs.

How the smart forecasting engine works

Once the data are verified and cleaned, they are fed into a custom neural network made of two tightly linked parts. One part is a dual‑channel structure that processes two streams of technical indicators in parallel, mimicking how biological neurons respond to pulses over time. This helps the model capture both short‑term jolts and longer‑term price trends across indicators like opening price, trading volume, and rate of change. The second part is a residual attention module that groups features and learns to "focus" more strongly on the most informative price and volume patterns while keeping training stable in deeper networks. On top of this, the authors use a "white shark" optimizer, a metaheuristic inspired by shark hunting behavior, to fine‑tune the network’s many parameters. This optimizer is designed to explore the search space widely at first, then zero in on promising regions, reducing the risk of getting stuck in poor solutions.

What the results say about real markets

The framework is tested on several years of daily data from the three exchanges, with earlier years used for training and the most recent year kept strictly for testing. Across markets that range from relatively calm (Hubei) to extremely volatile (Shenzhen), the model delivers high forecasting accuracy, with a coefficient of determination around 0.94 and relatively low average errors. It outperforms a long list of alternatives, including traditional deep learning models and state‑of‑the‑art Transformer‑based systems designed for long‑sequence forecasting. Careful ablation experiments show that removing any one component—noise preprocessing, attention mechanism, optimizer, or blockchain layer—weakens either predictive performance or governance‑related properties. Statistical tests confirm that the gains over competing models are unlikely to be due to chance.

What this means for the future of carbon markets

From a layperson’s perspective, this work offers a smarter and more dependable "weather forecast" for carbon prices. By combining data cleaning, pattern recognition, intelligent optimization, and secure tracking of data origins, the proposed system turns messy market records into more stable and interpretable price outlooks. While the current study is limited to three Chinese exchanges and historical data, the approach points toward forecasting tools that could help companies manage climate‑related financial risks, assist regulators in designing steadier carbon policies, and ultimately support a smoother transition to a low‑carbon economy.

Citation: Biswal, S., Kotecha, K. & Munjal, N. Carbon price fluctuation forecasting using an adaptive dual-channel residual attention neural network optimized with white shark optimizer and blockchain-based data provenance. Sci Rep 16, 13802 (2026). https://doi.org/10.1038/s41598-026-43184-6

Keywords: carbon markets, price forecasting, deep learning, blockchain data, climate policy