Clear Sky Science · en

Sentiment and stock price volatility: a multilayer heterogeneous graph network analysis of the new energy vehicle market

Why feelings matter for clean car stocks

The boom in new energy vehicles is not just about batteries, chips, and charging piles—it is also about how people feel. In this study, the authors show that the moods expressed in news reports and on online forums can push share prices of electric car–related companies up and down in ways that go beyond hard facts. By tracking how these waves of optimism and fear ripple through a tightly connected industry network, they explain why some firms become lightning rods for market swings and what regulators and investors can do about it.

Two voices that move the market

The paper focuses on two main sources of “market mood.” One is professional news—articles written and checked by editors that shape the broader information backdrop. The other is the stream of comments and posts from investors on an online discussion forum. The authors treat these as two distinct voices. News tends to be slower and steadier, while investor chatter is fast and emotional. Because the new energy vehicle sector depends heavily on policy, technology breakthroughs, and supply‑chain links, both voices are unusually powerful there. The study asks how these two forms of sentiment interact and, together, drive the sharp price swings seen in this industry.

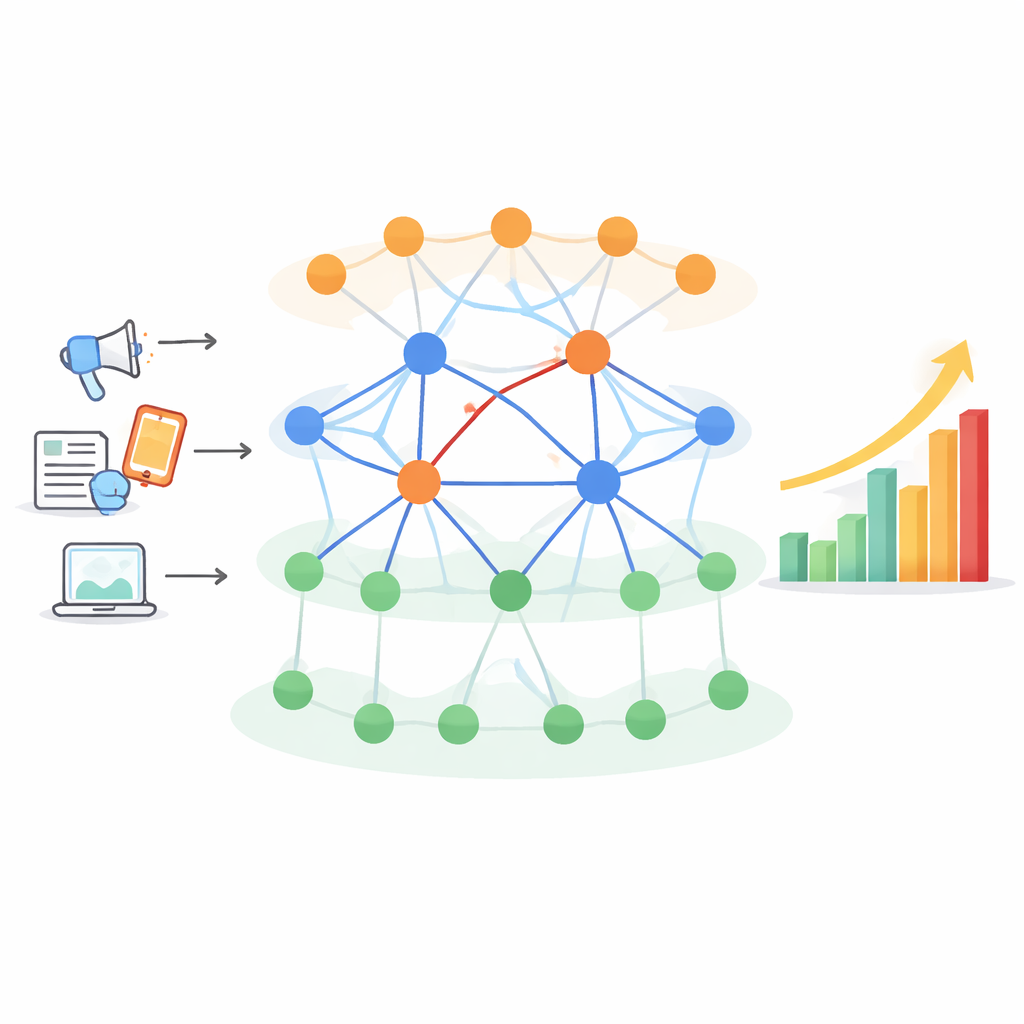

Following mood through a web of companies

Rather than looking at one firm at a time, the researchers build a network that links 24 major companies across the whole new energy vehicle supply chain, from raw materials and batteries to car makers and charging services. They collect about 80,000 news stories and 4 million investor comments from 2021 to 2024, score each item as positive, negative, or neutral using a fine‑tuned language model, and then average these scores day by day for each firm. Stock price changes are matched to the same daily grid. To capture both time patterns and cross‑firm links, the authors use a hybrid neural‑network design that combines tools for learning from sequences with tools for learning from networks. This allows them to trace how a burst of positive or negative tone in the news flows through investor reactions and finally into prices along the supply chain.

Slow news, fast crowds, and hub firms

The results reveal a clear division of roles. News sentiment changes slowly and exerts a gentle but lasting pull on expectations. Investor sentiment, by contrast, jumps sharply and has its strongest effect on prices within about three trading days. When forum mood turns sour, price drops are steeper than the gains that follow good mood, suggesting that fear bites harder than hope, especially in times of uncertainty. The impact is not spread evenly across the sector. A small number of central firms—large battery makers, leading car brands, and key service providers—act as hubs. Shocks that begin with news about these companies quickly trigger waves of concern or enthusiasm that pass through investors to many other stocks. A roughly one‑month window best captures how short‑lived emotional jolts and slower information shifts combine to move prices.

What this means for risk and rules

By mapping these pathways, the study links everyday chatter and headlines to systemic risk in a concrete way. It shows that markets do not simply absorb information; they amplify it through investor behavior and network connections. For regulators and exchanges, this implies that rapid clarification of major news—ideally within one or two trading days—and closer watch during the first three days after big announcements can soften destabilizing swings. Encouraging key hub firms to follow regular, transparent disclosure routines that fit natural monthly cycles can also reduce confusion. For investors, the findings are a reminder that crowded mood around a few star companies can quietly shape the fortunes of many others in the same chain.

A plain‑language takeaway

In simple terms, the paper concludes that in the new energy vehicle market, feelings are contagious and unevenly spread. Calm but persistent signals from traditional media set the background, while quick, sometimes frantic reactions from online investors deliver the immediate punch to prices. Because a handful of important firms sit at the center of the network, sentiment shocks that start there can ripple across the whole sector and make price swings larger than the underlying news might justify. Recognizing these patterns can help policymakers design better safeguards and help investors avoid getting swept up in short‑lived waves of excitement or panic.

Citation: Pu, Z., Yuan, X. & Zhang, Y. Sentiment and stock price volatility: a multilayer heterogeneous graph network analysis of the new energy vehicle market. Humanit Soc Sci Commun 13, 420 (2026). https://doi.org/10.1057/s41599-026-06661-x

Keywords: investor sentiment, media influence, stock volatility, new energy vehicles, financial networks