Clear Sky Science · en

Elite elimination osprey optimization algorithm optimized kernel extreme learning machine for bankruptcy prediction problems

Why spotting trouble early matters

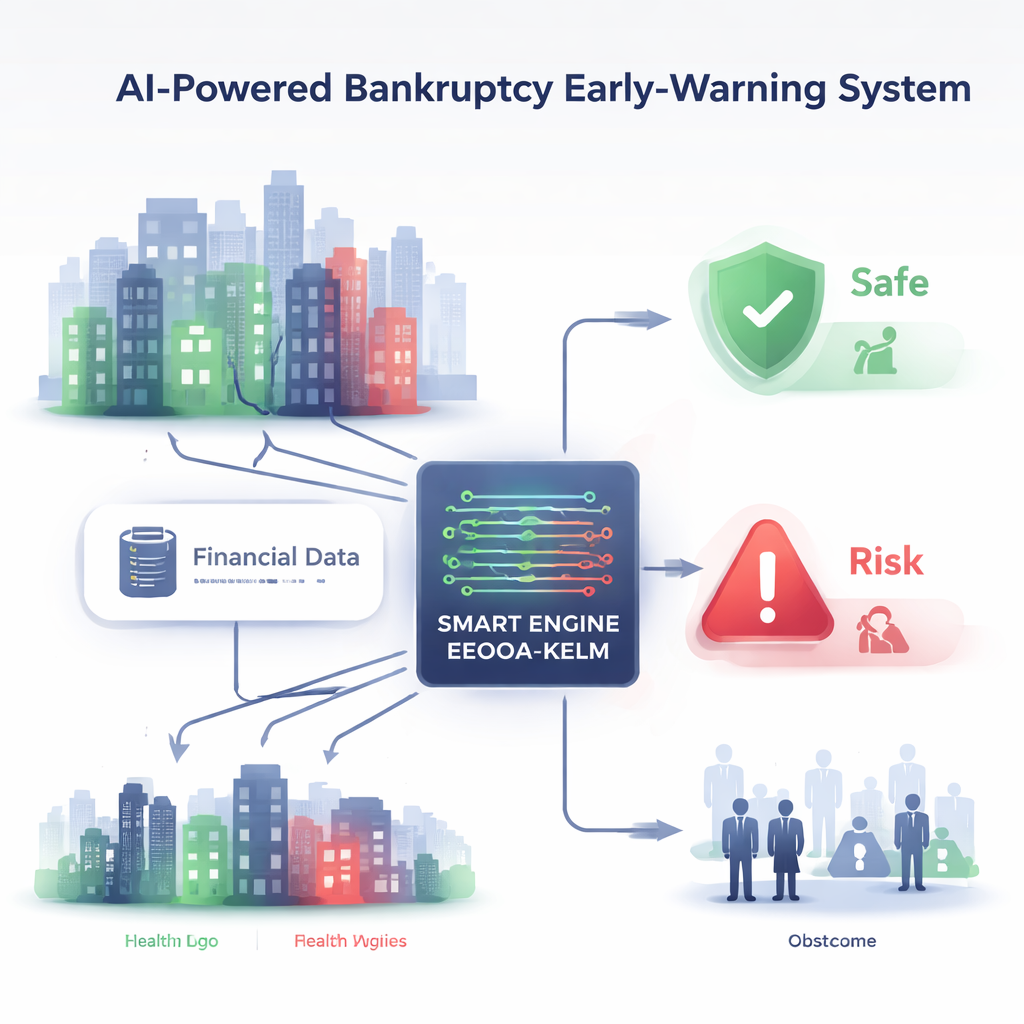

When a company goes bankrupt, the damage rarely stops at its front door. Workers lose jobs, suppliers go unpaid, banks and investors take losses, and entire regions can feel the shock. After recent crises and supply-chain disruptions, lenders and regulators urgently want tools that can warn them when a firm is drifting toward serious financial trouble. This paper introduces a new artificial-intelligence model that aims to do exactly that: sift through complex financial data and flag companies that are quietly sliding toward bankruptcy, more accurately and efficiently than many current methods.

Teaching computers to read financial warning signs

Traditional statistical models, and even older generations of machine learning, struggle with the messy, nonlinear nature of real financial data. Neural networks and support vector machines can capture complex patterns, but they often train slowly and can get stuck in "local" solutions that are not truly the best. A newer approach, called the Kernel Extreme Learning Machine (KELM), trains very quickly and usually makes strong predictions, but it has a catch: its performance hinges on choosing just the right settings for a handful of key parameters. Picking those settings by hand is difficult and can lead to overconfident models that fail when conditions change.

Nature-inspired search for better models

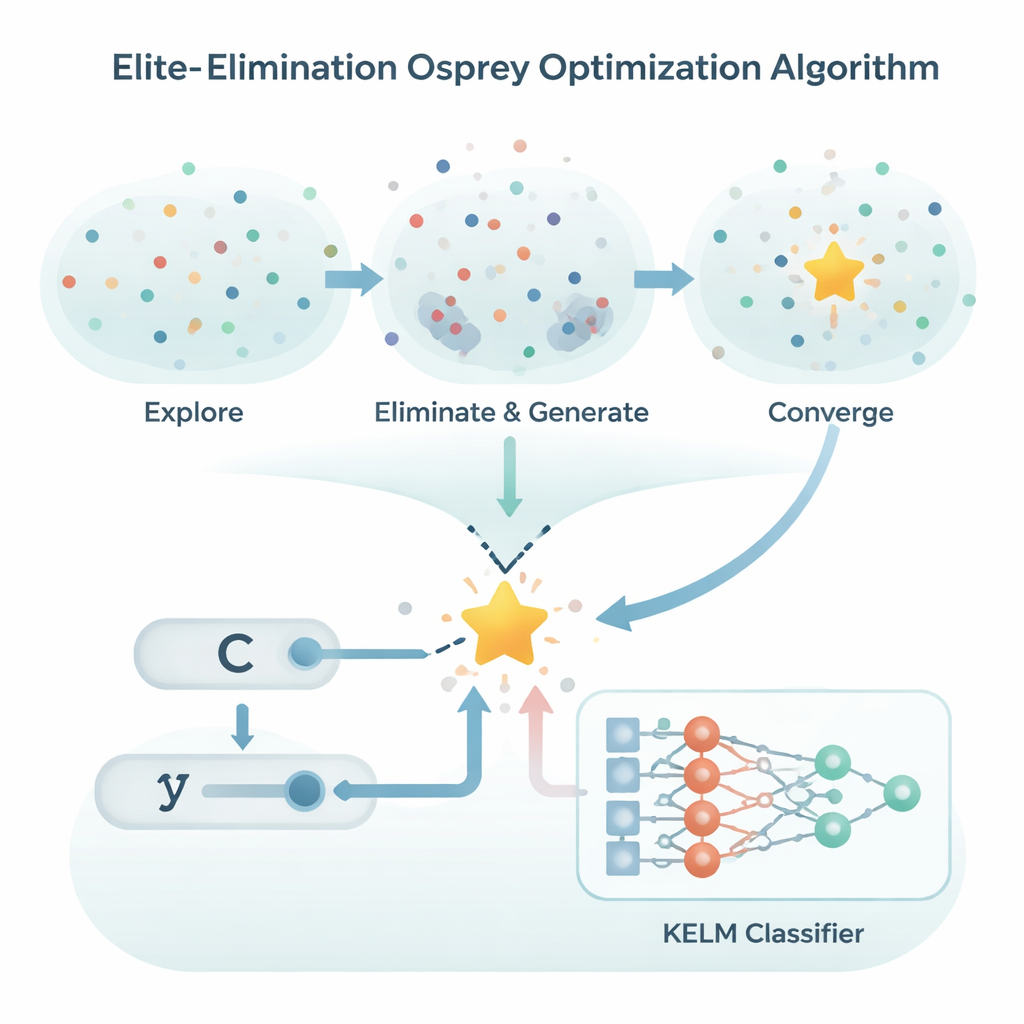

To tune KELM automatically, the authors turn to a class of algorithms inspired by animal behavior, which search for good solutions by moving a "swarm" of candidate answers around a landscape of possibilities. They build on a recent method modeled on the hunting habits of ospreys, a bird of prey. The new variant, called the Elite-Elimination Osprey Optimization Algorithm (EEOOA), adds three ideas: it lets the swarm learn mainly from its best members, uses a smart way of occasionally making large jumps to escape dead ends, and steadily removes weak candidates while generating fresh ones near the best solution found so far. A custom boundary rule keeps all candidates in promising regions instead of wasting effort on impossible or irrelevant values. Together, these tweaks help the search home in on high-quality parameter settings more quickly and reliably.

Proving the search works on tough test problems

Before trusting EEOOA with real financial decisions, the team first tests it on demanding mathematical benchmarks that are widely used to compare optimization methods. These functions are designed to be tricky, with many local peaks and valleys that can trap naïve search strategies. Across dozens of such problems in different dimensions, the new algorithm consistently converges faster and lands closer to the best-known solutions than seven well-known competitors, including Grey Wolf and Whale optimizers and the original osprey method. Detailed comparisons and ablation studies—where individual improvements are switched on and off—show that each of the three mechanisms adds value, and that together they provide the most stable and accurate search behavior.

Turning better search into better bankruptcy forecasts

Armed with this optimizer, the authors next build a full bankruptcy prediction system, EEOOA-KELM. They feed it a real-world dataset of 240 Polish companies, split between firms that later went bankrupt and those that remained solvent, described by 30 financial ratios such as profitability, debt load, and operating efficiency. For each round of testing, EEOOA searches for the best KELM settings by minimizing classification errors under strict cross-validation, a procedure that repeatedly reshuffles the data into training and test sets to avoid overfitting. The resulting model is then compared with versions of KELM tuned by other optimization algorithms. EEOOA-KELM achieves the highest scores across accuracy, precision, recall, and F1-score, while also showing the smallest variation from run to run—a sign of robustness rather than luck.

What this means for real-world risk monitoring

For non-specialists, the key takeaway is that the authors have built a more dependable early-warning engine for corporate distress. Instead of trying to guess which combinations of financial indicators and model settings might signal looming bankruptcy, they let a carefully designed search process explore the possibilities and lock onto those that perform best under repeated testing. On the sample of Polish firms, this yields modest but meaningful gains in correctly identifying troubled companies while avoiding false alarms. Although the study is limited to one dataset and country, the approach is general: with suitable data, the same combination of a fast-learning classifier and a refined, bird-inspired optimizer could help banks, investors, and regulators monitor financial health more accurately and react sooner when companies start to falter.

Citation: Liu, W., Wu, H., Wang, T. et al. Elite elimination osprey optimization algorithm optimized kernel extreme learning machine for bankruptcy prediction problems. Sci Rep 16, 6246 (2026). https://doi.org/10.1038/s41598-026-37249-9

Keywords: bankruptcy prediction, financial risk, machine learning, optimization algorithm, early warning systems