Clear Sky Science · en

LSTM-augmented vine copula modelling for energy-finance contagion analysis

Why Energy Shocks Matter To Your Wallet

When oil prices spike, green tech stocks soar or crash, and headlines warn of new tariffs or wars, those events don’t stay neatly in their own lanes. They can ripple through bank shares, retirement funds, and the broader economy. This paper asks a deceptively simple question: how exactly do shocks in global oil markets and fast-growing renewable energy stocks spread into the financial system, especially during crises—and can smarter, AI-assisted tools help regulators spot trouble before it snowballs?

Three Markets Tied Together

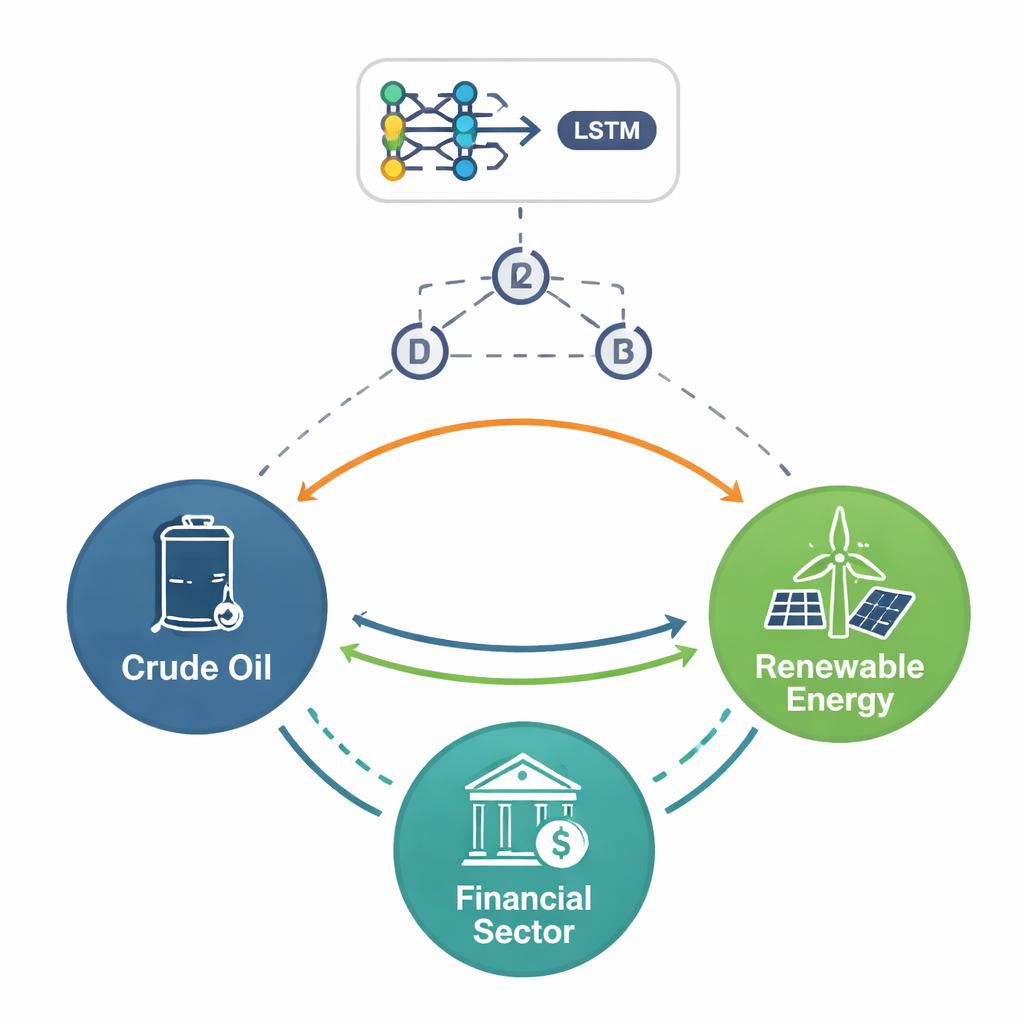

The authors focus on three closely linked arenas: traditional crude oil, China’s booming renewable energy sector, and China’s financial market. Using daily data from 2015 to 2025, a decade marked by stock crashes, the COVID-19 pandemic, wars, and trade conflicts, they show that these markets now move together in complicated ways. Oil still reacts sharply to geopolitical news, but renewables and financial stocks are increasingly intertwined, because green projects depend heavily on funding, investor mood, and supportive policy. When stress hits, losses in one corner can rapidly echo into the others, especially in the most extreme ups and downs rather than on ordinary trading days.

Following Risk At Different Speeds

To tease out these connections, the study does more than look at simple correlations. It first breaks market movements into short- and medium-term waves, filters out noise, and then examines how bursts of volatility cluster over time. This reveals that shocks in oil prices, renewable energy shares, and financial stocks behave differently across horizons. In the short run, all three can respond violently to news, but the financial sector shows particularly sharp reactions, jumping quickly and then slowly calming down. Over the medium term, swings are smoother but more persistent: bad news can keep markets on edge for months. Across all horizons, the authors find that extreme events—rare but severe booms and busts—occur far more often than a normal bell curve would suggest, making it crucial to focus on “tail” risks rather than average days.

Bringing AI Into The Picture

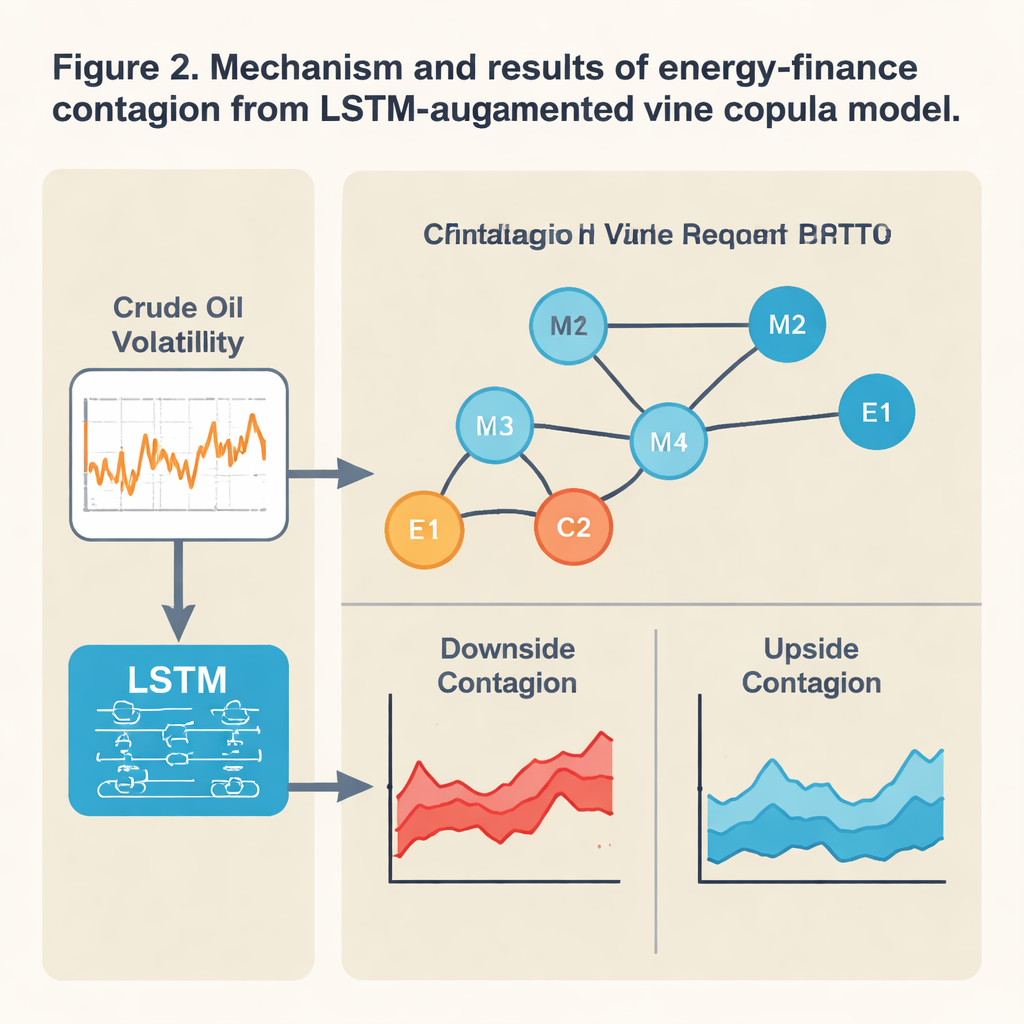

Traditional statistical tools often assume that relationships among markets are steady and mostly linear, which breaks down in turbulent times. Here, the authors combine a deep-learning model known as a Long Short-Term Memory (LSTM) network with a flexible dependence model called a vine copula. In plain terms, the LSTM scans recent oil price behavior to infer how “stressed” markets are likely to be tomorrow. That forward-looking stress signal is then fed into the vine copula, which maps how tightly the three markets’ extremes are linked at that moment. This pairing allows the strength and direction of connections to shift with conditions: when the model senses rising stress, it can show downside contagion—cascading losses—suddenly intensifying along particular routes, such as from oil and finance into renewables.

Downside Shocks Travel Faster Than Good News

Having built this AI-augmented framework, the authors track how risk spreads during major events like the 2015 Chinese stock crash, the 2020 pandemic, the 2022 Russia–Ukraine war, and renewed tariff battles. A clear pattern emerges: bad news travels further and faster than good news. Sharp drops in China’s financial and renewable energy markets strongly increase the chance of extreme losses in international oil, and vice versa. The link between renewables and finance is especially tight—the two often plunge together in crises. Meanwhile, the connection between oil and finance can flip sign: sometimes high oil prices hurt banks and stocks by raising costs and inflation, but under other conditions they move together, offering little protection for diversified portfolios. The model also shows that short-term contagion is more violent and uneven, while medium-term spillovers are steadier but still dominated by downside risks.

What This Means For Stability And Policy

For non-specialists, the bottom line is that energy and finance now form a tightly coupled system in which green assets play a central, and sometimes fragile, role. The study’s AI-enhanced approach does a better job than standard models at predicting when extreme joint moves are likely, especially in the tails of the distribution where crises live. That makes it a promising tool for regulators planning stress tests and for risk managers trying to understand how a sudden oil shock or policy change could ripple through banks and clean-energy investments. The authors argue that supervisors should treat the “green finance” chain—renewable projects funded by domestic capital—as a distinct source of systemic vulnerability, and design safeguards, such as targeted credit cushions and coordinated energy and financial policies, to keep future energy shocks from spilling over into full-blown financial crises.

Citation: Zeng, L., Huang, J. & Lin, X. LSTM-augmented vine copula modelling for energy-finance contagion analysis. Sci Rep 16, 5358 (2026). https://doi.org/10.1038/s41598-026-37150-5

Keywords: energy-finance contagion, oil and renewable energy markets, systemic risk, deep learning in finance, tail risk modelling