Clear Sky Science · en

Multiclass portfolio optimization via variational quantum Eigensolver with Dicke state ansatz

Why quantum ideas matter for your investments

Modern investors face a puzzle: how can you spread your money across many kinds of assets to balance risk and return, when the number of possible combinations is astronomically large? This paper explores how emerging quantum computers, working together with classical algorithms, might help tackle this challenge in a smarter way, especially for portfolios that must be diversified across several asset classes such as stocks, bonds, commodities, and cryptocurrencies.

The challenge of building a balanced portfolio

In real life, portfolio design is not just about chasing high returns or minimizing risk on paper. Large investors, from banks to pension funds, are required to diversify: they must hold a certain mix of asset types so they are not overexposed to any single sector or market swing. Mathematically, this turns portfolio design into a huge puzzle. Each asset is either included or not, and strict rules say how many assets must come from each class. The number of possible portfolios can be mind-bogglingly large, far beyond what a simple search can handle. Classical methods can solve small cases, but for larger, more realistic situations, they either take too long or give only approximate answers.

How quantum circuits enter the picture

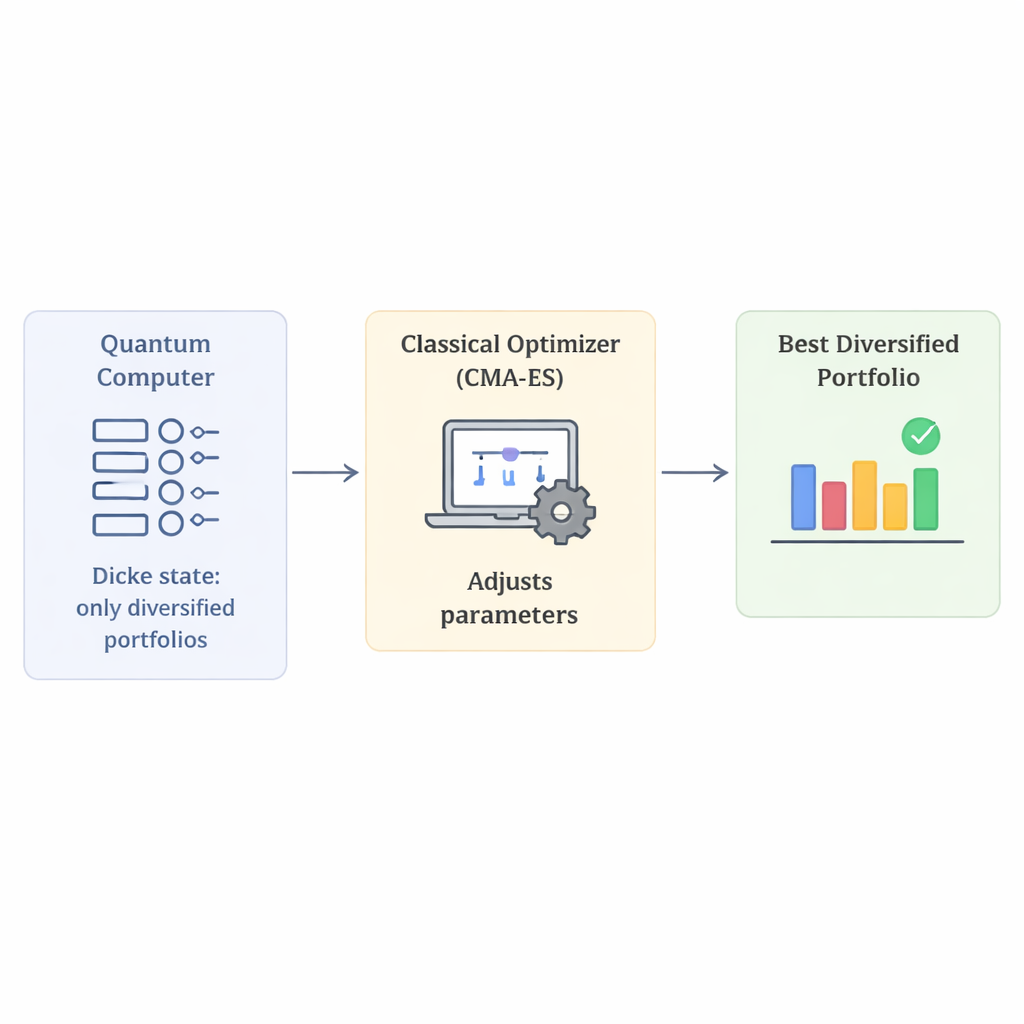

Quantum computers process information in qubits, which can represent many possible states at once. A family of methods called variational quantum algorithms aims to exploit this by preparing a quantum state, measuring it, and then using an ordinary computer to tweak the settings until the measured outcomes are as good as possible for the task at hand. In this work, the authors focus on one such method, the Variational Quantum Eigensolver. The key ingredient is the way the quantum state is prepared, known as the ansatz. A poor choice of ansatz wastes time exploring nonsense portfolios that break diversification rules; a good one steers the quantum search toward useful candidates.

A clever way to encode diversification from the start

The main innovation of this paper is to use a special family of quantum states, called Dicke states, to build portfolios that automatically obey diversification requirements. In plain terms, a Dicke state is a superposition over all combinations where exactly a fixed number of qubits are "on". If each qubit stands for choosing a particular asset, this means every candidate portfolio in the quantum state selects exactly the required number of assets. By combining several Dicke states—one per asset class—the authors create a starting quantum state that includes only portfolios with the right number of stocks, bonds, and other asset types. This design sharply shrinks the search space from all imaginable portfolios to only those that respect the rules, eliminating the need for artificial penalty terms that normally punish invalid choices.

Testing performance with simulated portfolios

Because today’s quantum hardware is still noisy and small, the authors test their approach using detailed simulations. They compare the Dicke-based ansatz against more standard constructions on portfolio problems of increasing complexity, using real market data obtained from public sources. For the classical side of the hybrid loop, they try several optimizers that adjust the quantum circuit parameters. Across their experiments, the Dicke-based method is more likely to hit the true best portfolio and achieves higher-quality approximations to the optimal solution. Among the tested optimizers, an algorithm called CMA-ES stands out: it finds the correct diversified portfolio more often and concentrates more measurement probability on that solution, especially when allowed to run for more iterations.

What this means for future investing technology

For a non-specialist, the key takeaway is that this work shows how to bake realistic investment rules—like diversification—directly into the fabric of a quantum calculation, instead of bolting them on afterward. By starting from a quantum state that already respects the constraints, the method wastes less effort and behaves more stably in tests. Although the study relies on simulations and does not yet claim faster performance than the best classical tools, it points to a promising route: specialized quantum circuits, paired with suitable classical optimizers, could one day help financial institutions navigate enormous, constraint-heavy portfolio problems that are difficult to handle today.

Citation: Scursulim, J.V.S., Langeloh, G.M., Beltran, V.L. et al. Multiclass portfolio optimization via variational quantum Eigensolver with Dicke state ansatz. Sci Rep 16, 6208 (2026). https://doi.org/10.1038/s41598-026-36333-4

Keywords: quantum computing, portfolio optimization, diversification, Dicke states, hybrid algorithms