Clear Sky Science · en

RF-LSTM carbon price prediction based on CEEMDAN decomposition and multiscale entropy reconstruction

Why carbon prices matter to everyone

When governments and companies pay for the right to emit carbon dioxide, the price of those emissions quietly shapes energy bills, investment in clean technologies, and even the pace of climate action. But carbon prices jump around in complex ways, driven by politics, weather, and markets. This study presents a new way to forecast carbon prices more accurately, helping policymakers, businesses, and investors better plan for a low‑carbon future.

Untangling a noisy climate market

Carbon trading systems, such as the European Union Emissions Trading System and regional pilots in China, were created to cut greenhouse gases at the lowest cost. In practice, their prices are anything but smooth: they react to changing rules, economic cycles, and shifting expectations. Traditional statistical models struggle with this kind of erratic, non‑stationary behavior. Even modern artificial intelligence tools like standard neural networks can miss important patterns or become unstable when prices swing sharply. The authors argue that making sense of such data requires first breaking the price history into simpler building blocks before applying advanced prediction tools.

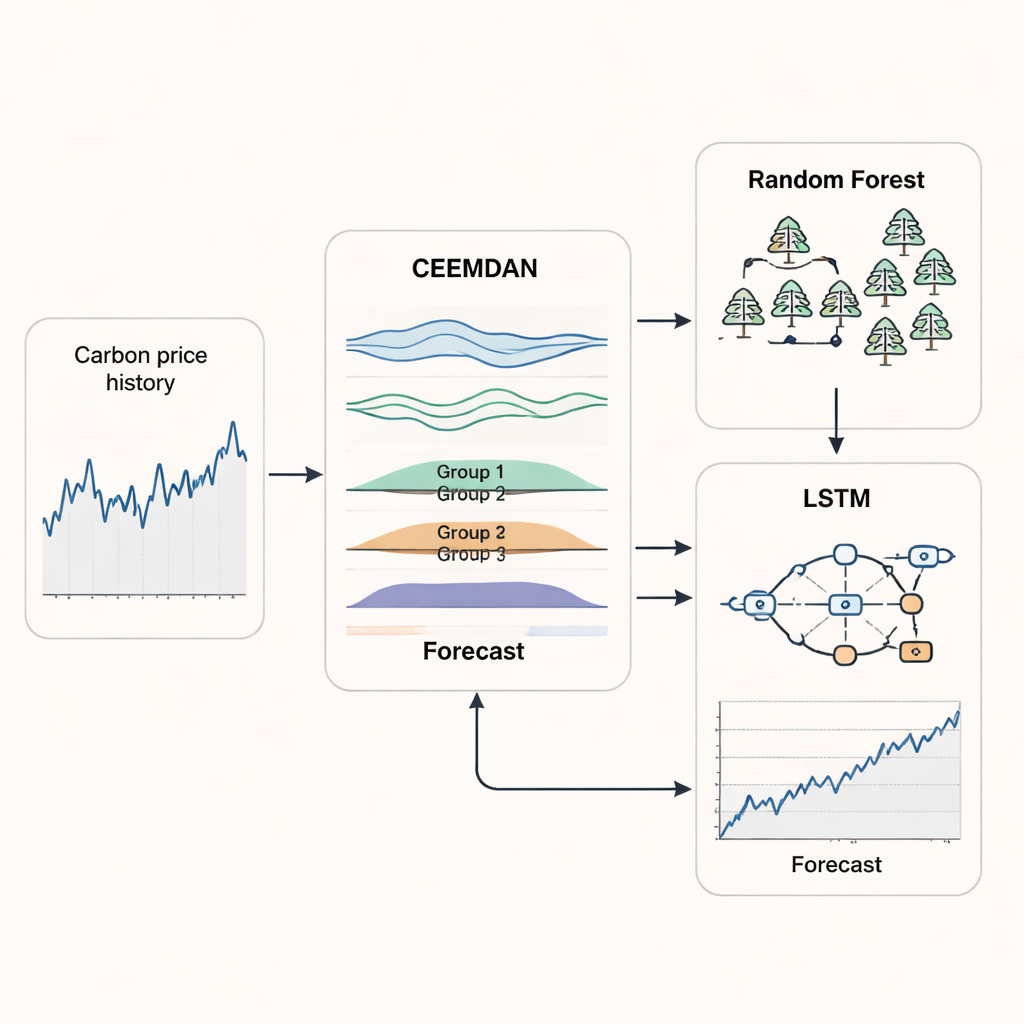

Breaking prices into hidden rhythms

The first pillar of the new approach is a method called CEEMDAN, which takes a jagged carbon price curve and decomposes it into several smoother components, each representing a different rhythm of movement—from rapid day‑to‑day jitters to slow, long‑term trends. Instead of treating all of these components separately, the researchers then use a measure called multiscale entropy to judge how complex each component is across different time scales. Components with similar complexity are grouped and reconstructed into a few clearer signals. This step reduces noise and redundancy, allowing the model to focus on patterns that truly matter for forecasting rather than being distracted by random fluctuations.

Pairing two machine learning brains

Once the carbon price series has been cleaned and regrouped, the study combines two machine learning methods that excel at different tasks. A random forest model—an ensemble of many simple decision trees—is assigned to the highest‑frequency group, where prices jump quickly and unpredictably. Random forests are good at capturing sharp, short‑term moves without overfitting. For the smoother groups that capture medium‑ and long‑term trends, the authors use a long short‑term memory (LSTM) network, a type of recurrent neural network designed to remember patterns over time. By letting each method specialize and then recombining their outputs, the hybrid RF–LSTM system aims to follow both the immediate twists and the broader direction of the carbon market.

Rolling with the market and testing performance

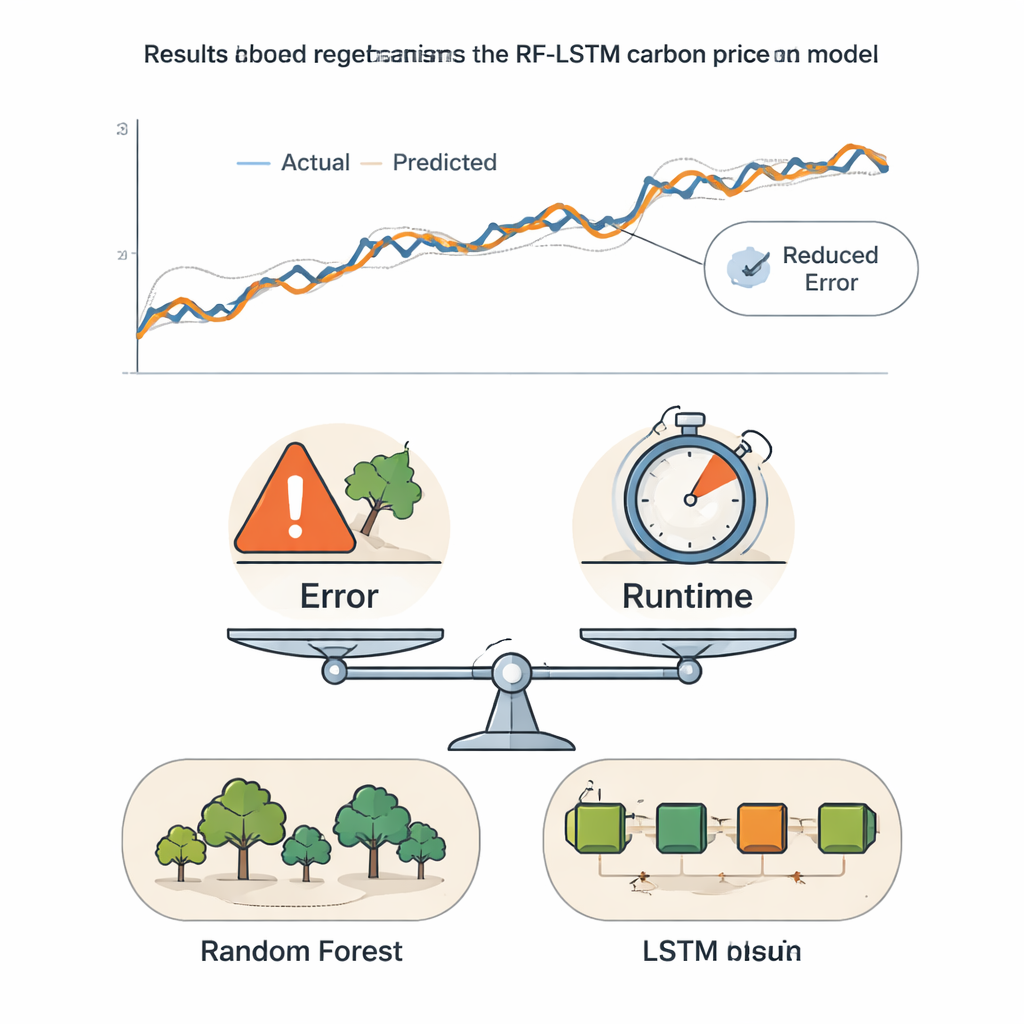

To reflect the way real‑world forecasting works, the authors adopt a rolling time‑window scheme. The model is trained on an initial stretch of historical data, makes a short‑term prediction, then shifts the window forward, repeating the cycle until it reaches the end of the series. This prevents the model from “peeking” at future data and allows it to adapt to structural changes in the market. The framework is tested on long time series from the Hubei carbon market in China and the EU system, using standard error measures and a directional accuracy index that counts how often the model gets the price movement—up or down—correct. The hybrid model consistently produces smaller errors and higher directional accuracy than a range of benchmark methods, including classic time‑series tools and more recent deep learning designs like Transformers and attention‑based networks.

Balancing accuracy and speed for real decisions

Because models that are extremely accurate can also be slow and costly to run, the authors introduce a composite score that blends prediction error with computing time. By adjusting how much weight is given to accuracy versus speed, they show when simpler models may be good enough and when the more sophisticated hybrid approach clearly pays off. In both the Hubei and EU markets, once accuracy is given even moderate weight, the new RF–LSTM framework comes out on top. For lay readers, the key takeaway is that this method offers a more reliable “weather forecast” for carbon prices, giving market participants and regulators a sharper, yet still practical, tool to guide investments, manage risk, and design climate policies.

Citation: Wang, H., Li, Y. RF-LSTM carbon price prediction based on CEEMDAN decomposition and multiscale entropy reconstruction. Sci Rep 16, 5230 (2026). https://doi.org/10.1038/s41598-026-35085-5

Keywords: carbon pricing, emissions trading, machine learning, time series forecasting, climate policy